What Is a Good Credit Score?

Credit scores are used to predict how likely a person is to pay their loans and credit card bills on time. Here are some facts about Credit Scores:

- People have more than one credit score, and scores can vary based on how, when and what information is used to calculate them.

- There are several Credit Scoring Companies Like FICO

- FICO indicates good credit scores fall between 670 and 739while another may indicate that good scores fall between 661 and 780.

Why Are There Different Credit Scores?

Credit-scoring companies use different methods to calculate credit scores. And they might weigh information in your credit reports differently as part of their calculations. That’s why your scores are likely to vary, even if just by a few points, when you compare them.

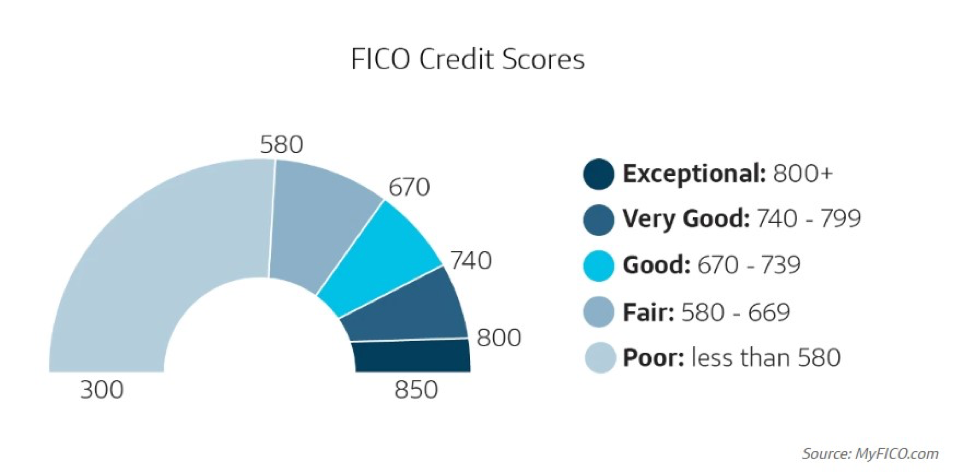

Credit Score Ranges

Below are some general guidelines for how being within a score range can impact your choices:

- A poor to fair score means you may find it difficult to qualify for many credit cards or loans. You might need to start with a secured credit card or credit-builder loan to build or rebuild your credit. And if you do qualify for an account, you may have to pay high fees and interest rates if you don’t pay your balance in full each month.

- A fair to good score means you may be able to qualify for more options, but you won’t necessarily receive the best rates or terms. You also might find you can qualify for a traditional unsecured credit card but have a harder time qualifying for a premium card.

- A very good or excellent score means you may be able to qualify for the best products with the lowest advertised rates. While creditors consider other factors too when determining your eligibility and rates, your credit score probably won’t be holding you back.

What’s a Good FICO Credit Score Range?

FICO scores that range between 670 and 739 qualify as good scores. Scores in that range are near or slightly above the U.S. average. FICO is used only as an explanatory example only. Their scoring models may be adjusted at any time.

What Affects Your Credit Scores?

So you can see credit-scoring models and credit reports are two big factors that determine your credit score. But if you don’t know what information from your credit report is being used, it’s not much help.

Here are a few factors the CFPB says make up a typical credit score:

- Payment history: How well you’ve done making payments on time. Late or missed payments can reduce your credit scores.

- Debt: How much current unpaid debt you have across all your accounts. This can include credit card debt, car loans and many other types of debt.

- Credit utilization rate: Reflects how much of your available credit you’re using compared with how much you have available. Credit utilization is usually expressed as a percentage.

- Loans: How many loans you have and what types of loans they are, such as revolving credit accounts or installment loans. Sometimes this is called your credit mix.

- Credit age: How long you’ve had your accounts open and have used credit. But remember, what qualifies as your oldest line of credit depends on what’s being shown in your credit reports.

- New credit applications: How many times you’ve recently applied for new credit. The effect on your scores might be minor, but a lot of new hard inquiries could still give a negative impression to lenders when they perform credit checks.

How Does FICO View Those Credit Factors?

FICO is specific about what it views as the most important credit factors. Payment history makes up about 35% of its scoring. About 30% is based on the total debt. The other primary factors are credit history (15%), credit mix (10%) and new credit (10%). These percentages can vary depending on what’s in your credit report, but they’re a good general guide.

What Information Do Credit Scores Not Consider?

Most credit-scoring models don’t consider information unless it’s part of your credit report. And even then, some parts of your credit report don’t impact your scores.

FICO’s and other scoring models don’t consider:

- Your age, race, nationality, color, sex, gender or marital status

- Where you live and work

- Your income, your job or whether you’re employed

- Whether you receive public assistance

- Political or religious affiliations

- The interest rates on your credit accounts

- Soft credit inquiries

Closed and paid-off accounts will stay on your credit reports and can continue to impact your scores until they fall off.

Why Is a Good Credit Score Valuable?

Credit scores are often associated with credit risk, credit cards, loan applications and other lending decisions. And having a good score could help you qualify for more financial products with better rates, terms and credit limits.

Even when you’re not borrowing money, good credit could help you. Good scores could lead to lower insurance rates and fewer and lower security deposits on things like telecom and utility accounts. And good scores may make it easier to rent a home, too. Your credit reports—but not your scores—could even impact some job prospects.

Using your Pre-qualification or Pre-Approval to improve Interest Rates and Credit Limits

If you’re approved for a loan or a credit card, a good credit score could mean higher credit limits, lower interest rates or both. And when you’re paying less in interest, you may have smaller payments and be able to pay off debt faster. In general, that means that higher credit scores could decrease the cost of borrowing money.

Be careful if you are shopping around for a loan. Be sure to understand that hard credit inquiries can affect your credit scores negatively.

Beyond Credit Cards and Loans

Good credit could affect other parts of your life, too:

- Landlords may check credit scores as part of rental applications.

- Some employers check credit reports before hiring job applicants.

- Insurers may consider credit to determine premiums.

- Cellphone and utility providers may waive security deposits if they see good credit scores.

How to Build a Good Credit Score

Building a good credit score really means using credit responsibly over time. The same is true when it comes to maintaining a good credit score. Here are five things the Consumer Financial Protection Bureau or the CFPB says you can do improve credit scores:

- Always pay your bills on time. To meet this goal, consider setting up automatic payments or electronic reminders to help you remember payment due dates.

- Stay below your credit limit. Experts recommend keeping your credit use below 30% of your available credit—across all your credit card accounts.

- Keep an eye on your credit history. Showing responsible credit habits over a long period can help your credit scores.

- Apply only for credit you need. If you apply for multiple credit cards and loans over a short period of time, lenders may think your financial situation has changed for the worse.

- Check your credit reports. Because your credit scores are based on the information in these reports, errors can hurt your credit scores.

Credit Score FAQs

How Can You Start Building Credit History?

There are a number of products to help customers who may be new to credit or trying to rebuild their credit. Many people start with a secured credit card, student credit card, credit-builder loan or student loan.

Is It Possible to Improve Your Credit Scores Quickly?

Building good credit can take time, but there are steps you can take to help improve your credit scores. If you have a high credit utilization ratio that’s hurting your credit scores, paying down your revolving credit account balances might quickly improve your scores. Or if there’s incorrect negative information in your credit report, disputing the error and getting it corrected right away could help.

Why Did My Credit Scores Change?

It’s common for scores to change somewhat throughout the month as creditors send the bureaus new or updated information about accounts. But figuring out what exactly caused the changes can be difficult.

If your scores suddenly dropped after you missed a couple of payments, you could assume that might have been the cause. But a slight increase or decrease could also be a normal result of your accounts aging—or new payments or updated balances being added to your credit report.

You may also see different scores depending on where you check your credit. Remember, scores depend on both the scoring model used and the credit report that the scores analyze. There are many different versions of FICO and VantageScore. And according to the CFPB, some lenders have their own custom credit-scoring models that they use to make credit decisions.

Your credit scores get created as a snapshot of your credit report when they’re requested. Any changes in the underlying credit report may lead to changes in scores, lower or higher.

Good Credit Scores

Using credit accounts and paying your bills on time can help you establish credit and lead to good, very good or excellent—credit scores. Avoiding late payments and having low credit card balances may also help you maintain good credit.

You want to consider using a credit-monitoring service to keep an eye on what’s in your credit reports and where your credit scores stand.